Business Articles - Employees

Articles & Tips

If you're not charging customers for all employee expenses, you're losing money

Labor is one of the most difficult costs to predict in an estimate. Basically, it's determined by calculating the hours required to complete a task or project, and then charging what it costs your business to compensate its field employees. But trying to predict the time required to complete a task or a project, especially if someone other than you will do the work, requires judgment and experience.

You can get unit costs for labor from a cost estimate book, but you have to be careful. The numbers in the book are unlikely to accurately reflect your own hard costs, even if you apply the regional adjustment factors provided. Your labor charges must reflect your company's actual expenses.

Consider that, if you pay each of your employees for 2,000 hours each year, and you fail to account for a couple of dollars per employee per hour, your loss could quickly become significant. Because no other company is exactly like yours, it's important to know precisely how much it costs your company to do business.

Burden and Benefits

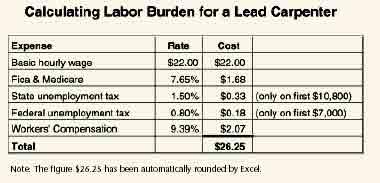

The hard cost of labor includes not only the hourly wage of the employee, but also all employer-paid taxes, Social Security, insurance, vehicle expenses, and any employee benefits (see the example given for a lead carpenter in Figure 1, next page). Workers' Compensation, liability insurance, auto insurance, paid holidays, vacations, medical benefits, education, employee meetings, cell phones, pagers, and every other labor-related expense must be factored into your hourly rates.

Overhead vs. direct costs. There are different schools of thought within the remodeling industry as to what should be considered overhead expenses versus hard labor expenses. Adding to the confusion, those items may be reinterpreted by your accountant, who likely views your business from the specific perspective of standard accounting practices.

Figure 1. The first step in estimating labor is to charge a rate that accurately accounts for your state and federal tax obligations and insurance requirements.

When evaluating labor costs, my rule of thumb is, "If you didn't have the project or the employee, would you still have the expense?"; If the answer is yes, then that expense should be assigned to your fixed over-head. But if your lead carpenter uses a cell phone specifically for work purposes, the phone bill should be considered a cost of labor for that employee. After all, if you let the employee go, assuming he or she is not replaced, would you keep the cell phone service? On the other hand, if you let that employee go, would you still have a fax line at your office? Most likely you would, so that expense would be assigned to your overhead.

When I pull an estimate together, I make sure that the hard cost of labor covers every cost I would incur in support of my field employees on that project. The total estimated cost is then marked up by a predetermined factor so that the selling price covers my overhead and profit.

Nonproductive Costs

An important consideration when determining the hard cost of labor is the difference between the hourly pay you give an employee and the hours that he or she actually works, producing income (Figure 2). When you add up all of the hours for paid vacations (2 weeks: 80 hours), holidays (5 days: 40 hours), paid time while attending training programs or trade events (12 hours total), as well as attending company meetings (2 hours every other week, or 50 hours annually), where will that money come from if you're not charging for it? Many remodelers I've worked with never realize that they're making this mistake. With 52 weeks in a year and a 40-hour work week, your company pays each full-time employee for 2,080 hours. The time paid for nonproductive hours, as listed above, totals 182 hours, or almost 5 weeks. Therefore, your company must collect enough money from 1,898 hours of production to pay that employee for 2,080 hours.

Don't forget sick days. If you pay, but don't collect for, sick days, you'll be losing vital revenue during a sick employee's absence. Even if you don't pay for sick days, you're spared paying the labor burden only on the basic hourly wage during the employee's absence. The cost of benefits and other annual expenses remains constant. To cover for these items, add an assumption for sick days, similar to that for paid vacation days, to your labor costs.

Figure 2. Paid vacations and other employee benefits put an additional burden on your billable hours. Subtract the annual total of these unbillable hours from the total hours paid in a year to find your total billable hours.

Individual Factors

To calculate the hard labor cost you should use when estimating or job costing,

you'll need to collect the expenses specific to each employee (Figure 3).

One may have a company vehicle; another may get a vehicle allowance. That may

create different costs for each, even if the two are paid the same hourly rate.

After you've assembled all of the expenses to support each employee for

a full year and added them to the employee's yearly wage, divide the total

cost by the actual hours worked. By doing that, you'll know what to charge

per hour in your estimates to cover your true costs. If you're not sure

which employee you'll assign to the project, use the highest-paid employee's

cost, and estimate the work based on his or her abilities and performance.

Dollars vs. Hours

Another trap to watch out for is how you job-cost labor and compare it to your estimate. When you compare your job cost information for actual labor against the estimated labor, be careful what you compare. You should be comparing the total dollar budget, not the number of hours. If you have different employees earning different wages, with different hard costs of labor, an hourly comparison will be inaccurate and will skew the value of your records.

Figure 3. To cover all of the costs associated with each employee, divide the total expenses by the actual hours worked. Add the result to each employee’s basic wage to find the hourly rates you should be using in your estimates.

Evaluate assumptions. If you job-cost a project using an incorrect labor rate from your estimate, you may be led to believe you're doing better than you are. If you've used the wrong assumption for the hard cost of labor, you'll either make more money than anticipated, or less. How many of us make more money than we budget for?

Here's a list of guidelines I use to determine hard labor costs:

• Create a computerized template that can be used for each employee.

• Use a worksheet to determine the costs for each employee, including office workers.

• Be sure that the figures you're using are accurate based on the current year's expenses.

• Be sure you're collecting enough money for the hours an employee actually works to cover what you will pay him or her for holidays, vacations, and other nonproductive benefits.

• Keep track of how you determined your labor costs. Verify your cost assumptions against changes during the year, and for next year, so you can update your labor costs accordingly.

• Check Workers' Compensation and employer-paid tax rates for any changes.

• Anticipate and add in employee raises during the coming year, in advance of selling the work to be completed after the raise.

• Assume an accurate cost per gallon for gasoline.

• Get accurate quotes for auto insurance from your provider.

• Consider creating a reserve account for vehicle replacement.

• Be clear on how you separate over-head expenses from the hard cost of labor expenses. You need to decide whether you'll recover overhead expenses through a charge to labor or a markup on your net costs.

• To help you verify or question how you determine your costs, ask your colleagues to share their costs and explain how they determine them.

by Shawn McCadden

Shawn McCadden is the president of Custom Contracting Inc., in Arlington, Mass., a regular speaker at JLCLive, and a co-founder of the Residential Design/Build Institute, LLP. Send requests for the MS Excel version of Shawn's employee worksheet to shawnm@designbuildinstitute.com.

This article has been provided by www.jlconline.com. JLC-Online is produced by the editors and publishers of The Journal of Light Construction, a monthly magazine serving residential and light-commercial builders, remodelers, designers, and other trade professionals.

Join our Network

Connect with customers looking to do your most profitable projects in the areas you like to work.